| After a seven-year boom, America’s auto industry is starting to feel like a déjà vu of the mortgage industry pre-crisis. You have consumers signing up for loans they can barely afford; investment banks rushing to securitize those loans to feed investor demand for higher-yielding products; lenders relaxing underwriting standards in order to generate more loans; shady loan officers inflating customers’ incomes and falsifying paperwork in order to justify bigger loans.

So, of course, things are turning ugly, especially in the nonprime sector of the car loans market. Default rates are rising; car values are falling; borrowers are suddenly finding themselves with underwater loans; recovery rates for lenders are plunging to below 50% in some cases.

Rising Default Rates

Total auto loans outstanding amounted to $1.19 trillion at the end of the second quarter of 2017, up almost 70% since a post-crisis trough in 2010. About 213 billion of that is nonprime, while 3.92% of the 1.19tn is seriously delinquent – meaning more than 90 days past due - up from 3.46% in Q2 2016. Delinquencies had fallen to near-record lows following the Great Recession, after auto lenders tightened approval standards. But, the down side of better performing loans for lenders was that volume fell since it was harder to get a loan. So, they proceeded to loosen underwriting standards to drum up car loan volume which, inevitably, resulted in an erosion of credit quality. Now, delinquencies are rising across the entire spectrum of credit scores, with the subprime and deep subprime segments deteriorating fastest. In fact, delinquency rates for deep subprime loans have ticked up to levels last seen in 2007. More data can be found in the New York Fed’s latest Quarterly Report on Household Debt and Credit.

Falling Used Car Values & An Inventory Deluge

The average used car lost 17% of its value in the past 12 months, a depreciation pace that is nearly twice that of 2014, when the annual rate was just 9.5%. Meanwhile, dealer inventories are at the highest level we've seen since the last financial crisis. It now takes an average of 75 days before a dealer is able to sell a new vehicle -- a data point that's also the highest since July 2009 when it took 80 days to make the sale. The situation will only worsen: Millions of car leases are set to expire over the next couple of years which will dramatically increase inventory in an already glutted market. One investment bank is projecting that used car prices could crash by up to 50% over the next 4-5 years.

Falling New Car Sales

U.S auto sales have been slowing for much of 2017, despite record spending on consumer incentives by automakers. The industry is expected to enjoy a temporary boost as consumers replace vehicles lost during this year’s spate of natural disasters, which would lift full year new vehicle sales to 17.1m from a previous forecast of 16.9m. However, barring an upside surprise, that would still mean car sales this year fell for the first time since the Great Recession, down from 17.55m last year.

Negative Equity on the Rise

U.S. consumers are more underwater on their auto loans than they have ever been before, as lengthening loan terms, rising transaction prices, and falling used car values take a toll. In the first quarter of 2017, one out of three trade-ins on new-vehicle sales had negative equity. The average amount of negative equity, at $5,195, was also a record high. Meanwhile, car loan payments are stretching to record lengths. The average loan term is about 70 months or nearly six years. Loans lasting 73-84 months have also increased, making up 32% of new-vehicle loan share in Q4 2016 versus 29% a year earlier. Used-car loans lasting 73-84 months accounted for 18% of the share, up from 16% a year earlier. The increase in loan durations is largely due to consumers getting more expensive cars with fancier tech, and lenders extending loan terms to get borrowers into an affordable monthly payment plan. Unfortunately, this often translates to higher loan-to-value and debt-to-income ratios, putting borrowers under greater financial strain.

Plunging Recovery Rates for Lenders

KAR Auctions is seeing a rising number of repossessions and expects nearly 2 million vehicles to be seized by lenders this year, up from 1.1 million at the nadir of the last recession. At the same time, the residual values of used cars have been plummeting because vehicles are depreciating faster than expected. That combination of higher defaults on the loans and lower recoveries on the cars is particularly painful for lenders, especially those with higher car-loan concentrations such as Capital One, Huntington Bancshares, Ally Financial or Santander Consumer USA. Data from Ally Financial shows that the lender got back about 60 cents on every dollar owed in April, from 72 cents a year ago. The recovery rate at Santander Consumer was even worse, dropping to 46 cents from 53 cents.

Given all this, lenders have started to pull back. The New York Fed reported that auto originations in Q2 2017 declined below the year-ago quarter, marking the second time only since 2009 that originations fell below the year-ago period. Origination volume in the subprime category fell the hardest. However, the pull back in financing can be a double-edged sword. When the financial crisis hit, retail auto sales collapsed to an annual rate of 7.9m in 2009, from 16m just 2 years earlier. One reason cited for the sharp decline was the reduced availability of auto loans.

New Theme Alert

MRP believes there is carnage ahead for the auto industry. Thus, we are adding SHORT AUTOS to our list of active themes. The negative outlook affects all segments:

Car companies not only have to contend with falling sales, but also any disruptions which may come out of the NAFTA renegotiations. Furthermore their marketshare is at risk of being cannibalized by tech companies entering the auto-making business, and by ride-sharing companies reducing the need for people to buy cars. Then there is the current scramble to produce electric vehicles and autonomous vehicles which means expensive retooling of factories and processes.

Dealerships and rental chains, both of which have to carry huge fleets of cars and trucks, are seeing their balance sheets tick down by the day as inventories become harder to move and car values drop.

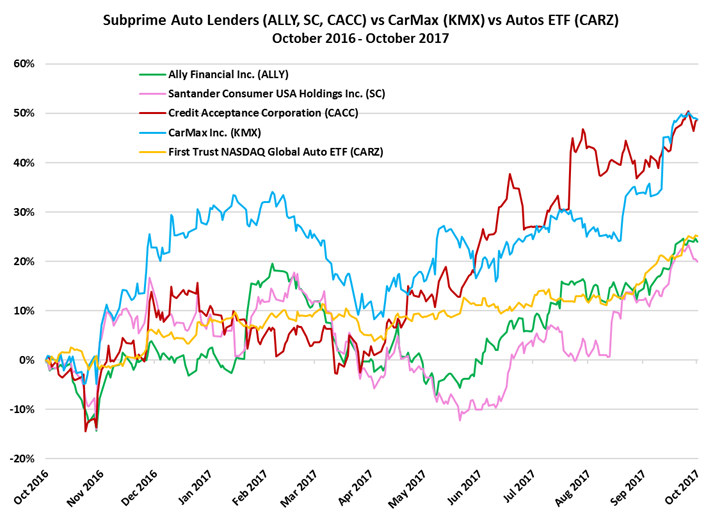

Lenders that get most of their revenues from auto loans and that have large subprime loan portfolios will suffer losses as delinquencies rise and recovery rates fall.

Auto asset backed securities (ABS) containing subprime loans will be affected as well. Last year, $26 billion of new subprime auto bonds were sold, topping average pre-crisis levels, and 10 times higher than the $2.5 billion sold in 2009. Moreover, the share of ABS tied to deep subprime loans rose from 5.1% of total subprime deals in 2010 to 32.5% in 2016, according to Morgan Stanley. In May, Moody’s drew attention to the fact that lender Santander verified incomes on just one out of every 10 loans it bundled into bonds. What’s more, a review by state authorities just a few years ago found that 10 out of 11 loan applications from a Massachusetts dealer contained inflated or unverifiable incomes. This means credit enhancements such as over-collaterization may not provide sufficient protection to bond holders.

Auto parts companies will be negatively affected by a slow down in the automotive industry and by the growing share of electric vehicles as a percentage of the total auto fleet. Electric engines have significantly fewer parts than internal combustion engines, so many specialized companies will find their products becoming obsolete over time.

Investors looking to short the entire auto industry, rather than specific segments, can do so with the First Trust NASDAQ Global Auto ETF (CARZ).

|

{kind=link}