|

|

|

|

|

|

|

|

| Joe Mac’s Market Viewpoint

Game-Changer Part II: Trumponomics Themes |

|

|

| The early December Viewpoint outlined our shift from an environment of stagflation to one of growflation, inspired by the surprise outcome of the 2016 presidential election. As promised, this follow-up edition expands on the impact of the disruptive Trump win on our thematic ideas and, will roll out several new ones that directly fall out from the changed environment. There is no doubt that the road ahead has unequivocally changed for the U.S. economy and the capital markets. Identifying change-driven themes is MRP’s mantra, and clearly, the U.S. presidential election was a game changer on many levels.

First, it seems the election outcome has influenced, not only investors, but the Federal Open Market Committee (FOMC) as well. As expected, the Fed boosted the fed funds target by a quarter point last week. But more importantly, this was the meeting in which FOMC members update the Summary of Economic Projections (SEP); new information on the expected path of interest rates was also released. Although the outlook for GDP growth, unemployment, and price inflation were similar to the prior quarter, the FOMC members did boost their expectations for the path of rates over the next three years.

The change was notable since the Fed has only been lowering expectations for some time now. After having pulled back over the past few SEPs on their expectations for the number of rate hikes expected in 2017, 2018 and 2019, the FOMC is now looking for three hikes rather than two in each of those years. True to form, the markets already show disagreement with the Fed. Although traders have moved up their forecast of the number of hikes for next year from 1 to 2, they are still one short of the new path the Fed has outlined. It seems to me that resolution of that disparity could dominate the performance of the markets at some point over the year ahead.

The extra dot that Fed officials have added to the outlook is not likely to derail equity investors’ enthusiasm for the Trump administration’s economic plans. But it may throttle it back for the time being. The Fed shift is likely to be more damaging to the fixed-income markets than equities. In the meantime, the relative performance of investment themes should persist.

New Themes

Energy & Energy Services & Equipment

MRP remains very positive on the energy sector overall. Indeed, the energy theme continues to be one of our favorites in the post-election environment. But if the Trump GDP growth goals of 3-4% come anywhere close, the demand acceleration for energy will be considerable. The U.S. is still the world’s top oil consumer and revved up economic growth will mean big gains in energy consumption. In the short-to-intermediate term, even though U.S. production seems to have stopped falling, the just-announced OPEC cutbacks will help constrain global supply. Our expectation that crude prices would rise to $60-$80 by the spring of 2017 remains intact.

Longer-term, however, the $60-$80 range may become a ceiling on prices as attention in the US turns more and more toward new drilling and exploration. President-elect Trump has said that he plans to “unleash an energy revolution”. Specifically, his website states that the new administration’s vision is to unleash America’s $50 trillion in untapped shale oil and natural gas reserves, plus hundreds of years supply of coal reserves. The plan includes “onshore leasing of federal lands, eliminate moratorium on coal leasing, and open shale energy deposits.” Obviously, if all elements of the plan were enacted, a lot of oil would get produced which would be great for U.S. energy independence. It could, however, lead to another glut of U.S. oil which would constrain the price.

Still, it is highly unlikely that much, if any, of the plan would take effect in the very near term. Most of the production in question would be hitting the market years from now. For that reason, we are currently thinking that $60-$80 target for crude oil is still attainable in the year ahead, but that range could be a ceiling down the road. Thus, our current thinking is that the energy sector of the market remains attractive and we expect prices to rise further as the supply/demand imbalance is corrected.

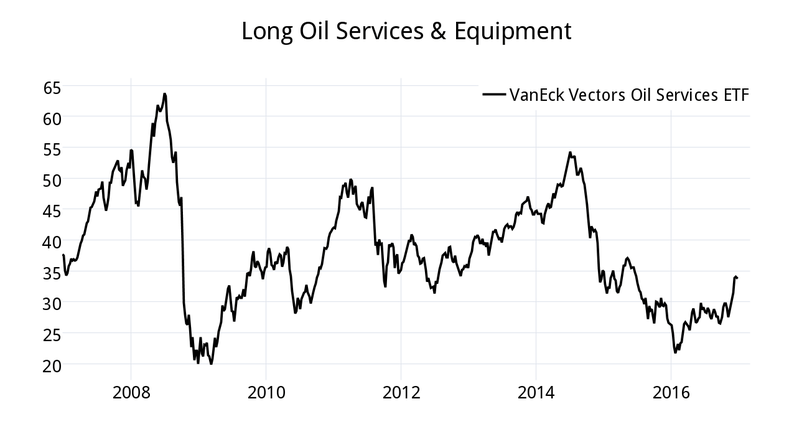

Our focus, however, is now shifting toward companies that specialize in the exploration, drilling, transferring of oil, and oil-related product (e.g. LNG, gasoline), as well as companies that manufacture oil-related equipment – such as the names in the OIH. We are adding energy services and equipment as a new theme, which we will be tracking via the VanEck Vectors Oil Services ETF (OIH).

|

|

| Infrastructure and Capex

Trump’s plans to rebuild the nation’s infrastructure will have profound implications for several very specific industry groups in the United States. Trump has said that, as President, he would “rebuild our highways, bridges, tunnels, airports, schools, hospitals,” an effort that “will put millions of our people to work.” The problem we have with the directly-related themes is that many pure-play stocks have already run up dramatically prior to the election on expectations of strong fundamentals resulting from the 2015 Highway Bill signed into law just a year ago. Some asphalt and cement producers are already sporting multiples that are typical of biotechs or social media giants — selling at 30-40 times next year’s earnings estimates.

Nonetheless, the broad sector of capital spending-sensitive issues, when combined with other features of the Trump plan, could be poised for several years of outperformance. From building the wall with Mexico, to imposing tariffs on imported goods (like steel), to the infrastructure rebuilding program, and the proposed tax cuts on individuals and corporations, plus the plan to re-patriate billions of corporate dollars held overseas — all suggest there will be substantial increases in demand for industrial materials and machinery. In particular, there is a provision in the Trump plan to allow a 100% write-off on plant and equipment investments, which if adopted, would pull forward a lot of future spending.

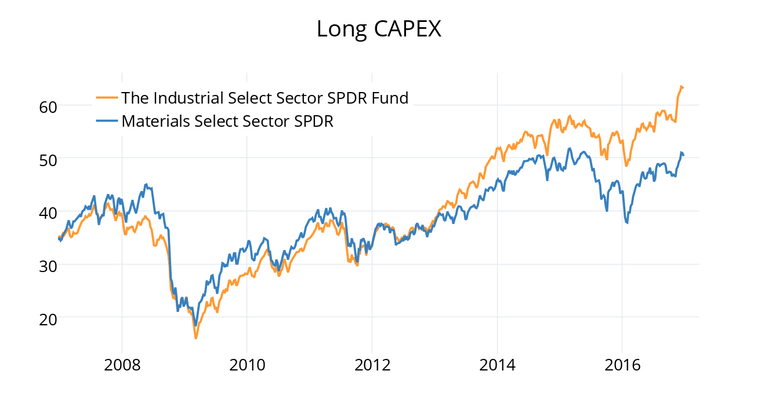

Obviously, engineering and construction companies would benefit as well but many of these are more dependent on corporate capital spending than on public infrastructure. Broader improvement in cash flows could result from other aspects of the Trump proposals. Improved corporate cash flows resulting from lower taxes and higher growth rates could spur a boom in private sector non-residential construction outlays. So, with this report we are adding capital spending as a new MRP theme. Industrials (XLI) and Materials (XLB) are two of the 10 main sectors of the S&P that should outperform over the next few years, driven by a resurgence in overall capital spending, and we are adding both as new themes.

|

|

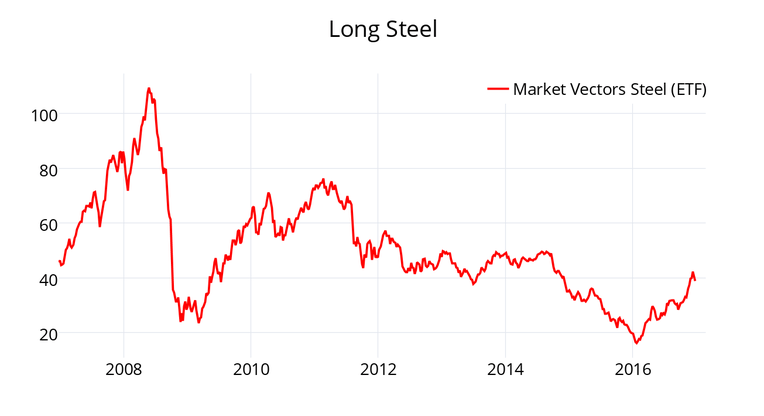

| On a more granular level, the steel industry could be a much bigger winner percentage-wise, and so we are adding Steel (SLX) as a theme for more aggressive investors. |

|

| Financial Services

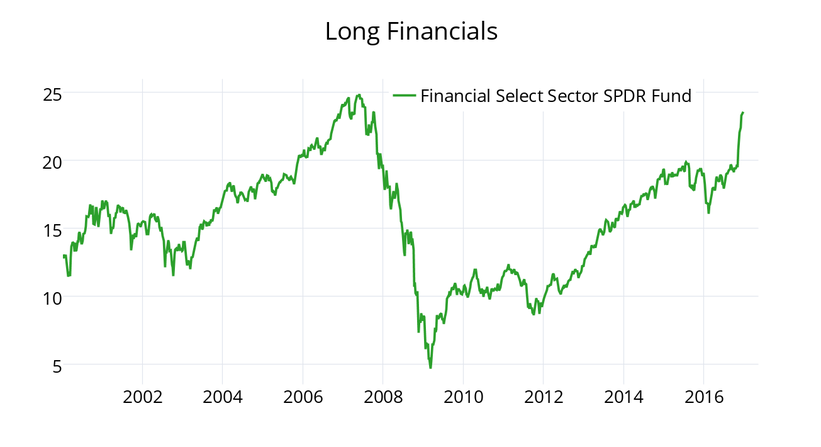

Under the Trump administration, the environment over the next several years should also be particularly good for the fundamentals of the financial services industry – in particular, the banks. Rolling back onerous regulations imposed over the past decade would be an obvious positive. In addition, changing expectations about the interest-rate and inflation outlooks has already resulted in a steepening of the yield curve and that is likely to continue. Lastly, if the new administration is successful in accelerating the US GDP growth rate, that should be reflected as well in an acceleration in loan demand. So, fewer regulations, better spreads, and stronger volume growth would add up to a greatly improved environment for banks and financial services in general. We are, therefore, adding the financial sector of the economy as a new Trump Victory theme. One way to gain exposure to the theme is through the Financial Sector SPDR ETF (XLF). |

|

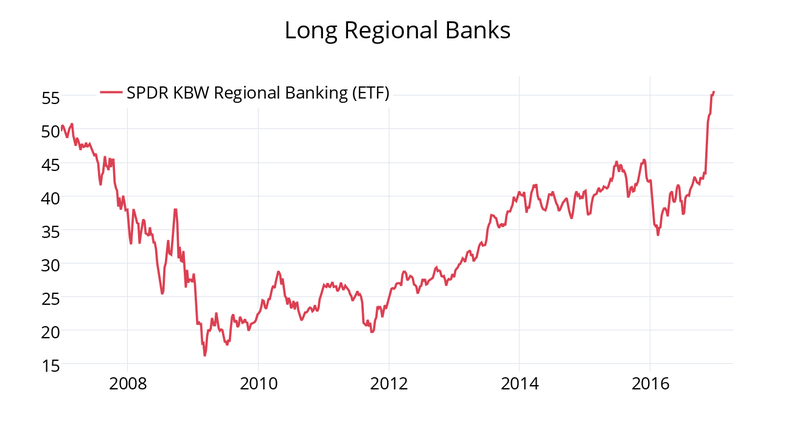

| Within the banking sector, regional banks should be major beneficiaries. We are adding the group as one more new theme and will track it through the SPDR S&P Regional Banking ETF (KRE). |

|

| The bottom line is that we remain bearish on bonds, we continue to think value stocks will trump growth stocks, and energy is still a favorite sector. Moreover, we are adding oil services, capex plays, and financial services as new MRP themes. We will be monitoring the progress of these new themes with the OIH, XLI, XLB, SLX, XLF, and KRE ETFs. Many of the stocks included in these sectors and industries have had very strong rallies since the election. We are surprised at how quickly the share prices have moved, and had been hoping for a pullback before launching these new themes. Nonetheless, it seems to us that the upside potential over the next few years could be multiples of what has happened so far and, therefore, we are launching the themes effective with this report. |

|

|

|

|

|

|

|