|

|

|

|

|

|

|

|

| Joe Mac’s Market Viewpoint

Running Hot: Time for TIPS, Gold, Energy, EM & Value |

|

|

| Janet Yellen got investors’ attention recently. Speaking at a conference in Boston, the Federal Reserve Chair described the potential benefits of temporarily running a high-pressure economy, what one pundit labeled “running hot”. She clearly outlined “plausible ways” that a hot U.S. economy could reverse some of the adverse effects of the Great Recession with robust demand and a tight labor market.

Perhaps Yellen was just speaking hypothetically. In fairness, the idea was indeed framed that way in her speech. On the other hand, maybe she was laying the groundwork for continuing on a very gradual path toward interest rate normalization, even in the face of what are likely to be surging inflation numbers over the next six months.

Reverting back to the good old days of “Fedspeak” — the use of language by central bankers that is incomprehensible to the average Joe — Yellen spoke about hysteresis, heterogeneity, and representative-agent models. But her bottom line was that some of the long-term damage done by the financial crisis could be undone by pursuing an economic environment that in the old days would be described as overheating. |

|

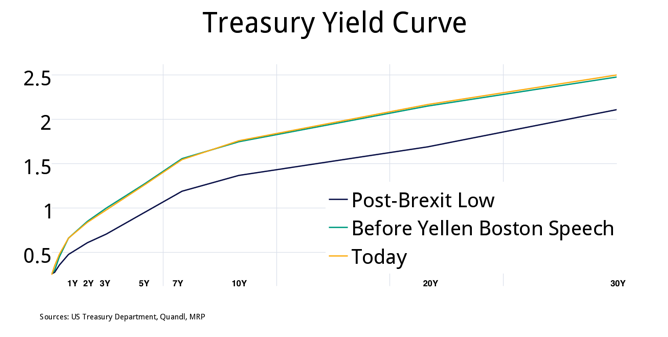

| The capital markets took notice. Equities sold off initially, but then rebounded, and the yield curve, which had already been steepening, steepened slightly further.

At MRP, we continue to believe the U.S. economy is on the verge of a multi-year period of stagflation — a macroeconomic environment of continuous subpar secular growth accompanied by sharply higher inflation, but peppered by periodic growth surges for a few quarters or so. As it happens, the three months just ended looks likely to be one of those real growth surges: GDP growth for Q3 2016 could be more than double the average of the first two quarters.

Meanwhile, headline inflation is in the process of surging. At this time last year, the CPI was bumping along around a year-over-year (“YoY”) change of zero; it’s now 1.5% and may soon surpass the Fed’s 2% inflation target by a considerable margin. The dramatic fall in energy and other commodity prices, earlier in this cycle, has masked overall inflation pressures. The Core CPI, which strips out volatile food and energy components, shows core prices have already breached the Fed’s target, rising 2.2% YoY as of September. A more granular breakdown of the Core CPI reveals that services inflation has surged to 3.2%. Even the most recent reading of the Core PCE Deflator Index, the Fed’s preferred measure of inflation, shows that index is at 1.7% YoY as of August, already hitting the FOMC’s projection for the full year 2016. But now, crude oil prices have risen over 80% from their February 11th lows and other commodity prices have begun rising as well. We expect many other hard goods prices to head much higher in the coming year, stoking higher inflation numbers.

If one merely assumes oil prices remain flat for the next year and then calculates the YoY change, the yearly change in oil prices would have a shocking surge. From the lows in February, the YoY change in oil prices would soar from -45% to +80% by early 2017. Energy accounts for only around 7% of the CPI, and it does not gyrate as wildly as crude oil, about half of the energy sub-index being electricity. But most of the other half is fuel oil, which swings almost as crazily as crude. The surges are so huge, that oil prices remaining flat from here would mean a headline CPI that could be sporting a high 2-handle print by the coming winter, other things being equal. The impact would dissipate by late spring 2017 as YoY comparisons fall to zero, unless, of course, oil prices rise further. In fact, MRP estimates oil will have a dramatic further rise to the $60-80/bbl range, maintaining the upward pressure on the overall CPI. |

|

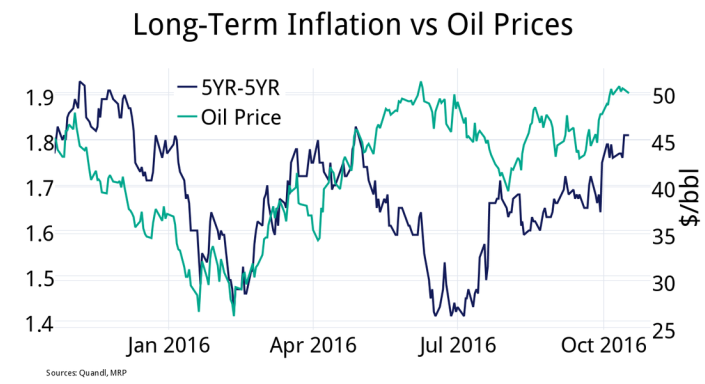

| And now, inflation expectations are also creeping up. Curiously, inflation rates for the five-year period beginning 5 years from now seems to be strongly influenced by changes in the spot price of oil from 2 nanoseconds ago. When crude prices were plunging into the high $20s, the inflation expectations for 5 years from now plunged as well. And now, with spot oil prices having risen to around $50 since the mid-February low of $28, traders’ expectations of what inflation will be in the five year period beginning five years from now have risen accordingly.

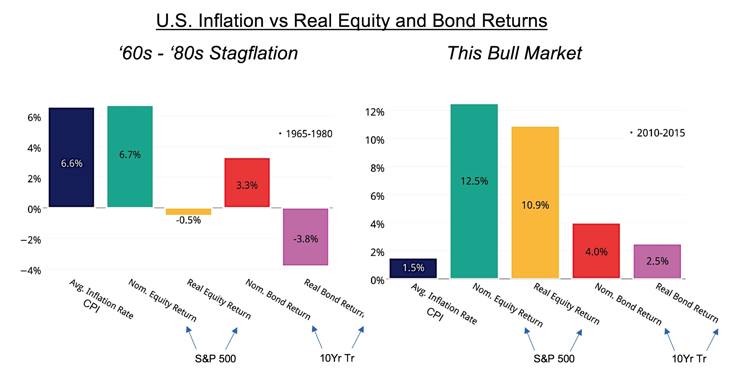

So, the Fed running a hot economy is not likely to produce hot returns from the major asset classes. A return of stagflation, even for a while, is NOT widely anticipated by investors and could be quite disruptive to capital market prices. Historically, a stagflation environment has not been great for equities and bonds. For the fifteen years ending 1980 – the last time the U.S. experienced stagflation – nominal annual returns from common stocks averaged 6.7%. But when inflation was subtracted, the real returns were -0.5%. For bonds, nominal yearly returns were 3.3%, but real returns were -3.8%. During that same period gold prices soared as investors flocked to inflation-protected assets. Energy and technology also performed well.

Looking forward, fixed-income market returns are likely to be, at best, lower than recent coupon rates. However, if ever there was a time to initiate a position in treasury inflation-protected securities (TIPS) – a recently launched MRP theme – this is it. Ways to do so would include:

- The iShares TIPS Bond ETF (NYSEARCA: TIP) tracks the performance of the Barclays U.S. Treasury Inflation Protected Securities TIPS Index, which is composed of TIPS with maturities ranging from 1 to 20+ years.

- The Vanguard Short Term Infl-Prot Secs ETF (NASDAQ: VTIP) tracks the performance of the Barclays U.S. Treasury Inflation Protected Securities TIPS 0-5 Year Index, which is composed of TIPS that mature in less than 5 years.

For those who believe rates will rise and prefer a bigger payout than just inflation protection, the ProShares UltraShort 20+ Year Treasury ETF (NYSEARCA: TBT) might be the way to go, although, it is not for the faint of heart. Longer-term bonds perform poorly in rising interest rate environments, and the TBT allows investors to gain leveraged inverse exposure to U.S. treasuries with a remaining maturity of at least 20 years.

The broad U.S. equity market, is not likely to deliver anything even close to the same nominal and inflation-adjusted returns as it has produced over the past five years and could experience a lot of volatility. |

|

| Yet, even in a broad capital market decline in stocks and bonds, there are always some securities that will outperform relatively, if not absolutely. As we wrote recently, for example, the S&P 500 can be divided between value stocks and growth stocks. For over eight years, growth had handsomely outperformed value; but it looks to us as though that trend has begun to reverse, and value should outperform growth by a wide margin for the forseeable future. The present value of future earnings growth will be revised down when interest rates rise, affecting growth stocks disproportionately; value stock sectors should smartly beat growth as rates one way or another go higher.

We maintain our value over growth stocks theme. The rise in U.S. inflation will likely lead to the continued rolling over of the U.S. dollar. Gold and gold mining stocks, an MRP theme since October 2015, should continue to advance as an inflation-hedge. Emerging market equities, added as a theme almost a year ago, were very negatively impacted by the dollar’s earlier strength, and should continue to benefit from further U.S. dollar weakness. Moreover, the energy sector is poised to benefit from higher prices in the near-to-intermediate term. As the global thirst for crude oil rebounds in emerging economies such as India and China, and from record breaking miles driven in the U.S., the ability of the supply side to meet demand will become increasingly strained, creating an oil shortage and higher prices. An OPEC agreement to cut production will only add to the upward price pressure. Energy is a theme we added in early April. Lastly, it is clear that rising Fed Funds will eventually push up mortgage rates. Some will argue that rising mortgage costs will be a headwind for the U.S. housing sector, but we would argue that powerful demographic forces will overshadow that negative.

Election Impact

There are now less than 2 weeks to go until the U.S. presidential election. The polls clearly favor Hillary Clinton, the Irish and UK bookmakers are showing dramatic odds in her favor, and the media has all but declared her already victorious. However, it is important to remember what the polls were saying about Brexit and the Columbian/FARC Treaty. It ain’t over until it’s over. Moreover, there is as always the issue of the down-ballot voting and the resulting future make-up of Congress.

Nevertheless, some clients have asked how the election outcome might affect our stagflation story. The simple answer is no one knows; indeed, no one ever knows what the future will bring. There are clear differences between the two leading candidates on many issues that will directly affect the economy: trade, tax policy, government regulation, and healthcare, to cite a few. But it is past and current monetary policy that has sown the seeds of the current inflation upsurge, and it will be future monetary policy that will determine future inflation. So, we can look at where the candidates may stand based on comments they’ve made and/or the views of policy makers who are said to be on their respective short lists for top market and economic jobs.

Janet Yellen’s term expires in February 2018. The democratic platform calls for governance changes that would increase diversity and remove career bankers from the leadership of the regional Fed banks. Although Clinton has not specifically said she would reappoint Yellen, our guess is that she would or bring in someone new with similar or even more dovish views about the path to interest-rate normalization. In this case, the “running hot” scenario would be more likely to materialize. Trump, on the other hand, has said that as president he would replace Yellen. If he were to appoint a hard-money hawk, U.S. monetary policy might take a more restrictive turn in 2017. As a result, we would likely see a tight-money induced market drop, similar to what happened in the early ‘80s, but less inflation down the road.

|

|

|

|

|

|

|

|