|

|

|

|

|

|

|

|

| Joe Mac's Market Viewpoint Time for Value |

|

|

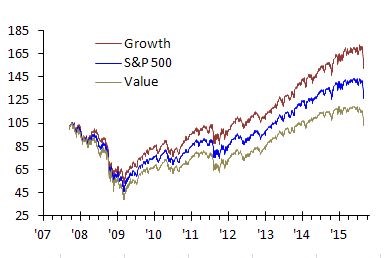

| It is one of the most spectacular market cycles in history. Not only has the S&P 500 tripled in price from the cycle low in March 2009, it has also soared 37% past its pre-crisis levels in 2007, to new record highs. That headline story, however, masks a style bifurcation that has endured throughout the 8-year down-up ride: Growth stocks within the index have almost consistently outperformed their Value counterparts …. and by a wide, wide margin. The performance chart of Growth versus Value tells it all. However, unfolding macro environment suggests that a turning point may be at hand.

Chart I: Growth vs Value |

|

| Source: Bloomberg, McAlinden Research Partners

To begin with, the S&P 500, the Russell, and other market indexes all have many sub categories, according to size, industry, and style characteristics. In the latter case, the constituents of the index are grouped into Growth or Value buckets. Revenue growth, price-to-earnings ratio (P/E,) and market price momentum determine if a constituent belongs in the Growth bucket. For Value, the key variables are price-to-book value, price-to-sales, and P/E. In this discussion, we focus on the S&P Growth and Value sub-indexes.

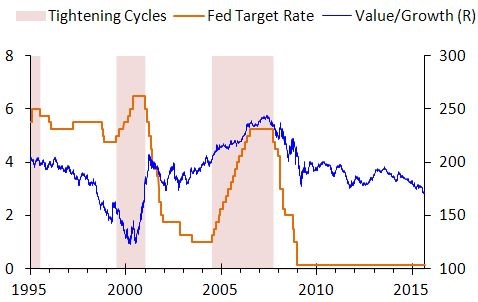

There is a single macroeconomic event on the horizon that could drive a reversal of the Value over Growth underperformance: the imminent end of the Federal Reserve’s zero interest rate policy (“ZIRP”.) After 8 years of falling or zero rates, the Fed is now ready to begin a process of raising rates back to normal levels which presumably would be dramatically higher than zero at the short end and well above the current 2% of the 10-year Treasury. There are both theoretical and empirical reasons for expecting the end of ZIRP to be the catalyst for a reversal in the Growth/Value relative strength.

The price of securities is theoretically based on expectations of future streams of cash discounted back to present value. In such a calculation, the discount rate is a critical input. For more rapidly growing companies, which by definition are expected to have much higher levels of earnings way down the road, the more distant cash flows have a greater current value when interest rates are unusually low, as they have been for years now. Although the timing of the Fed’s first hikes and the steepness of the path to higher rates is still being debated, there is little argument that higher rates are on their way. As the Fed tightens monetary policy, the discount rate applied to future streams should rise as well. This recalibration process will hurt growth companies disproportionately.

Chart II: Growth over Value During Fed Cycles |

|

| Source: Bloomberg, McAlinden Research Partners

Empirical evidence adds further support: the forgoing simple reasoning is borne out by a look at previous business cycles. In contrast with the prevailing wisdom that a hike in the fed funds rate will be a negative for Value stocks, history shows that Value has typically outperformed Growth during periods of rising interest rates. For instance, leading up to the financial crisis, rates started rising in mid-2004 from 1.00% and continued upward until reaching 5.25% two years later where they stayed until September 2007. Value outperformed throughout that period, until just a few months before the Fed started cutting rates as the financial crisis unfolded.

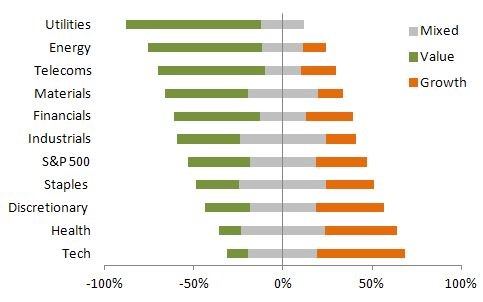

Chart III: Growth vs Value Across Sectors |

|

| Source: Bloomberg, McAlinden Research Partners

Our review of the constituents in the Value and Growth categories is summarized in Chart III. There are companies in what might be thought of as Value sectors that are included in the Growth Index, and there are companies in the Value Index that are actually in growth-type businesses, with quite a few issues being classified as a little bit of both. Investors seeking Value names will find them more often in the Utility, Energy, Telecom, and Financials space. Growth names are more typically found among Consumer, Healthcare, and Technology segments.

The global rout of stock prices has left some investors in shock. But it must be said that, it was long overdue. Conditions had been building for some time, as the transition to a rising rate environment has gotten closer. The first double digit correction has now occurred. But this sell-off is most likely not over and could get much worse before year-end. We have been saying that it wouldn’t surprise us to see a percentage decline that begins with a 2 or 3 before the correction ends. Moreover, we think the Long Value / Short Growth trade even works in a market decline of that magnitude, but really gets legs as stocks recover. A prolonged period of Value beating Growth, then, may soon be underway. |

|

|

|

|

|