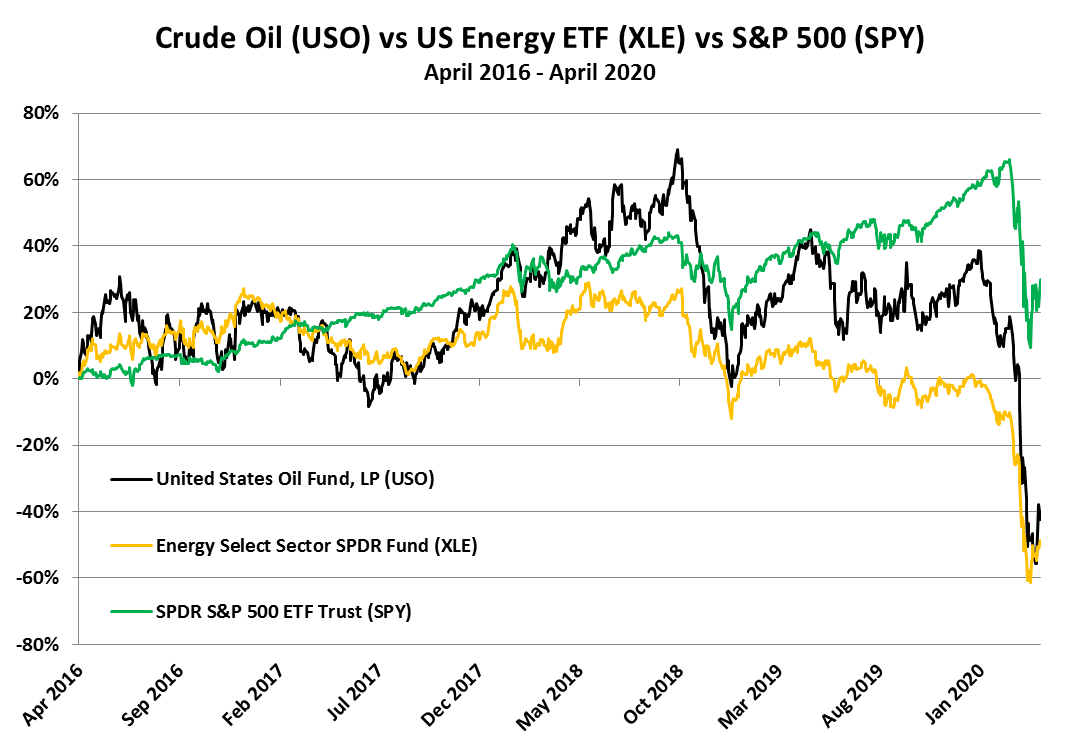

Due to the ongoing spread of Coronavirus, worldwide oil demand has dropped by roughly 30%, or about 30 million barrels per day (bpd), at the same time that Saudi Arabia and Russia have been flooding markets with extra supply.

Though the Russians walking away from their partnership with OPEC, and the with output cuts that had gone along with it, was enough of a shock to send crude oil prices tumbling, a real price war had not ensued until Saudi Arabia also vowed to boost their own oil output well above 10 million bpd, an increase of 300,000 bpd from levels at the time. According to Bloomberg, the Kingdom told some market participants it could raise production much higher if needed, even going to as high as a record 12 million barrels a day. After talks with Russia broke down, Riyadh immediately began slashing its so-called official selling prices, offering record discounts of $6-$8 per barrel.

Saudi Arabia’s end goal is to assert their dominance in world markets, eventually bring Russia back to the table. In undercutting prices for Russia’s crude and flooding international markets, the Kingdom believed it could nullify Russian efforts to increase their exports.

It looked like both sides were digging in for the long haul. Saudi Arabia’s breakeven costs are astronomically low compared to most other oil producing nations outside of the Gulf and the Financial Times reported that Russia was prepared to draw from its $150 billion national wealth fund in order to boost budgetary spending, while oil prices remained at between $25 and $30 a barrel. The Russian government said the country could maintain that level of budgetary support and cover the lost revenue for the next 6 to 10 years.

However, as oil plunged more steeply than anyone predicted, with Brent crude hitting an 18-year low of $20 in March, it appears both sides have already blinked.

Last Thursday, almost out of nowhere, US President Donald Trump unleashed a tweet that promised a joint cut of 10 million bpd, “and maybe substantially more”, from Saudi Arabia and Russia, sparking a 25% rally in crude spot prices. Russian President Vladimir Putin echoed the Trump tweet, telling his country’s top oil executives that oil producing countries should join together to slash output by 10 million bpd to reverse the collapse in world oil prices. Kirill Dmitriev, CEO of Russia’s sovereign wealth fund RDIF, has told CNBC that the Russia and the Saudi Kingdom are indeed “very, very close” to a deal on oil production curbs, easing some skepticism that crept into markets over the weekend. 10 million bpd would be equivalent to about 10% of current global production.

The two nations will resume talks on Thursday via video conference. The original meeting was scheduled for last weekend, but some lingering disagreements meant ironing out a deal on decreased production would have to wait. The 10 million bpd figure may not be an immediate and exclusive measure for Russia and Saudi Arabia, rather something the two countries would build up to, while recruiting other oil-producing nations to join the cuts.

Bloomberg reports that Russia, for instance, is prepared to chop as much as 1 million bpd off of their current levels right off the bat, but wants the US to join into the agreement and take an equal amount of their own production off the market as well. Meanwhile, Saudi Arabia has called on Western European and North American producers to join the production adjustment effort. Norway will be attending the Thursday meeting along with representatives from Alberta, Canada’s deeply troubled oil province.

The day after Thursday’s summit, the Financial Times reports G20 oil ministers are expected to hold a separate emergency meeting after a push by Saudi Arabia and the International Energy Agency. The meeting would mark the first time the G20 has specifically convened to address energy issues, showing the depth of concern about the oil crash. The rotating presidency of the group is currently in the hands of the Kingdom, giving them some sway over the group’s discussions on the topic of oil markets.

While the US has not laid out any mandates for cutting domestic crude production, and could find it difficult to do, given the country’s antitrust laws, output is expected to fall, deal or no deal with other oil producing nations. Most of the gains the US has made in oil production over the last decade have been through “tight oil” from shale basins, acquired through high-cost fracking. Shale producers, most of which budgeted for oil between $55 per barrel and $65 per barrel in 2020, have moved quickly to idle rigs, cut staff and generate cash for expenses.

Over the past 2 years, MRP has reported a number of times on the inability of US shale to turn a meaningful profit, just last month highlighting an accelerated pace of bankruptcies in 2019. Worse, upwards of $200 billion of North American oil-and-gas debt maturing over the next four years was certainly going to push more firms into bankruptcy, with or without Coronavirus cutting crude prices in half. Speculative-grade, or subinvestment, debt makes up more than 60% of the total to be repaid between now and 2024, “implying a higher degree of default risk for the industry”, said Moody’s, the rating agency, in a February report.

Though the industry withstood a price war initiated by Saudi Arabia back in the mid-2010s through sizable financing deals and cash injections from investors, that same support will not exist in 2020 and the industry must finally focus on prices, not production, for profitability. While President Trump has sought to help the industry through fiscal stimulus or slapping tariffs on US oil imports, nothing has materialized yet.

Signs that declines in output are on the horizon are already beginning to show. Total US stockpiles of crude oil (excluding strategic petroleum reserves) hit an 11-month low last month, per weekly EIA data. In the final week of March, total inventories were 2% below 2019’s peak. Total rigs engaged in the exploration and production of oil and natural gas in the United States totaled just 664 in the week through April 3, compared with the prior-week count of 728. The current national rig count is already below well below the 1025 total rigs online at this time last year.

Though smaller shale-based drillers will struggle to adjust to ultra-low prices, larger oil companies will have some options if declines in US production do materialize.

As Reuters notes, larger US oil producers like Exxon Mobil Corp. can leverage their scale and diversified resources to turn a profit at much lower costs than smaller shale-dependent producers. Exxon’s oil is profitable at $26.90 per barrel on its New Mexico properties, which are about a quarter of its Permian holdings, according to Rystad. By cutting production, Exxon and others would be able to eliminate their most inefficient wells and focus on bringing down their average breakeven costs. The company has already reported it would slow its development in the Permian Basin, the largest US shale field that spans Texas and New Mexico. Occidental Petroleum Corp., and privately held CrownQuest Operating, both have costs below $30 per barrel. |