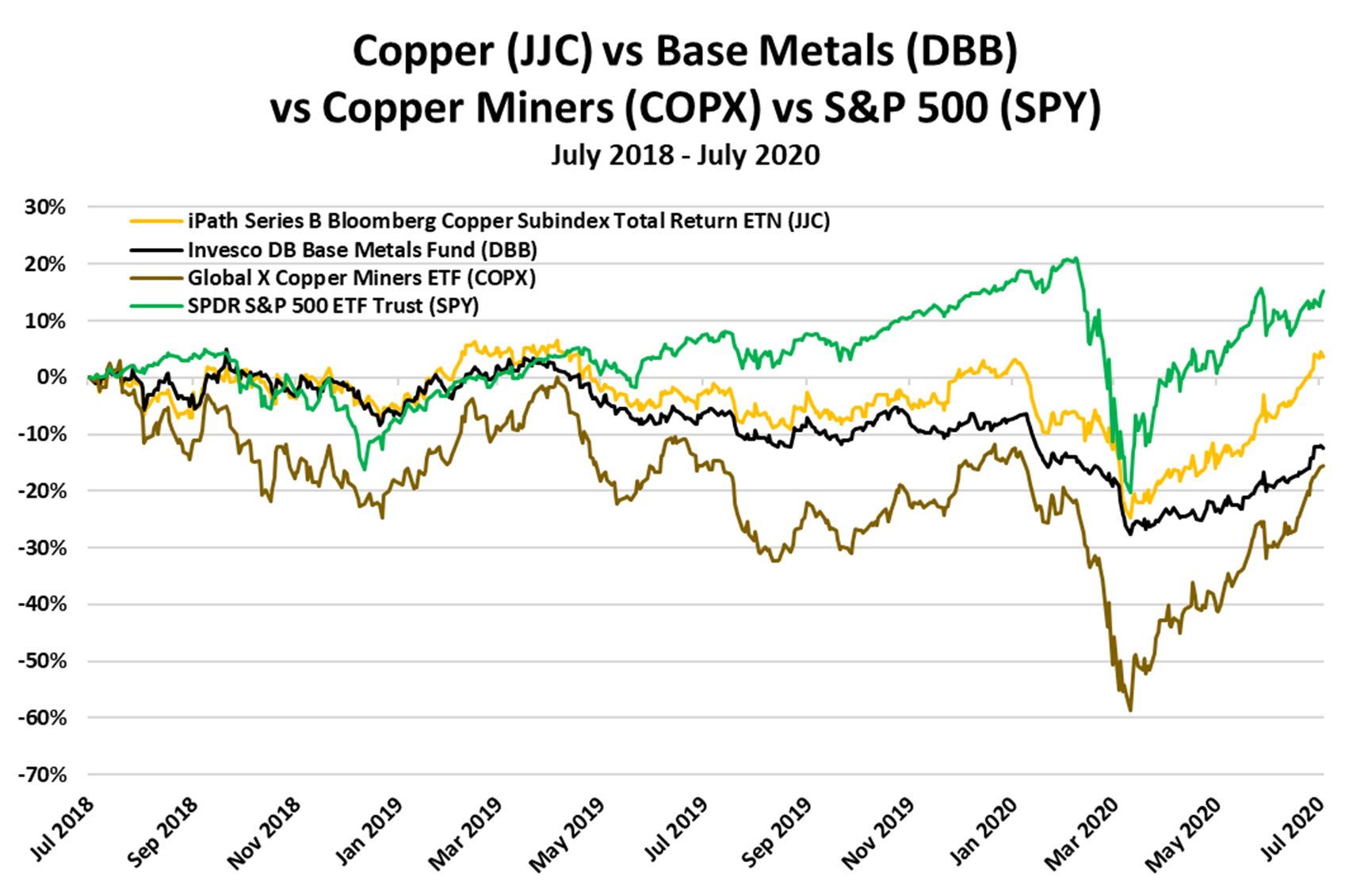

In our February Market Viewpoint titled “Post-Coronavirus Commodities Comeback”, MRP made the case that historically cheap commodities were likely to explode in 2020, aided by the virus’ deteriorating foothold in China, the upcoming changing of the seasons, and the eventual need to restock empty warehouses once economic activity resumed. Our expectation that the U.S. dollar would start depreciating again was an additional consideration, given that commodity prices have an inverse relationship with the greenback.

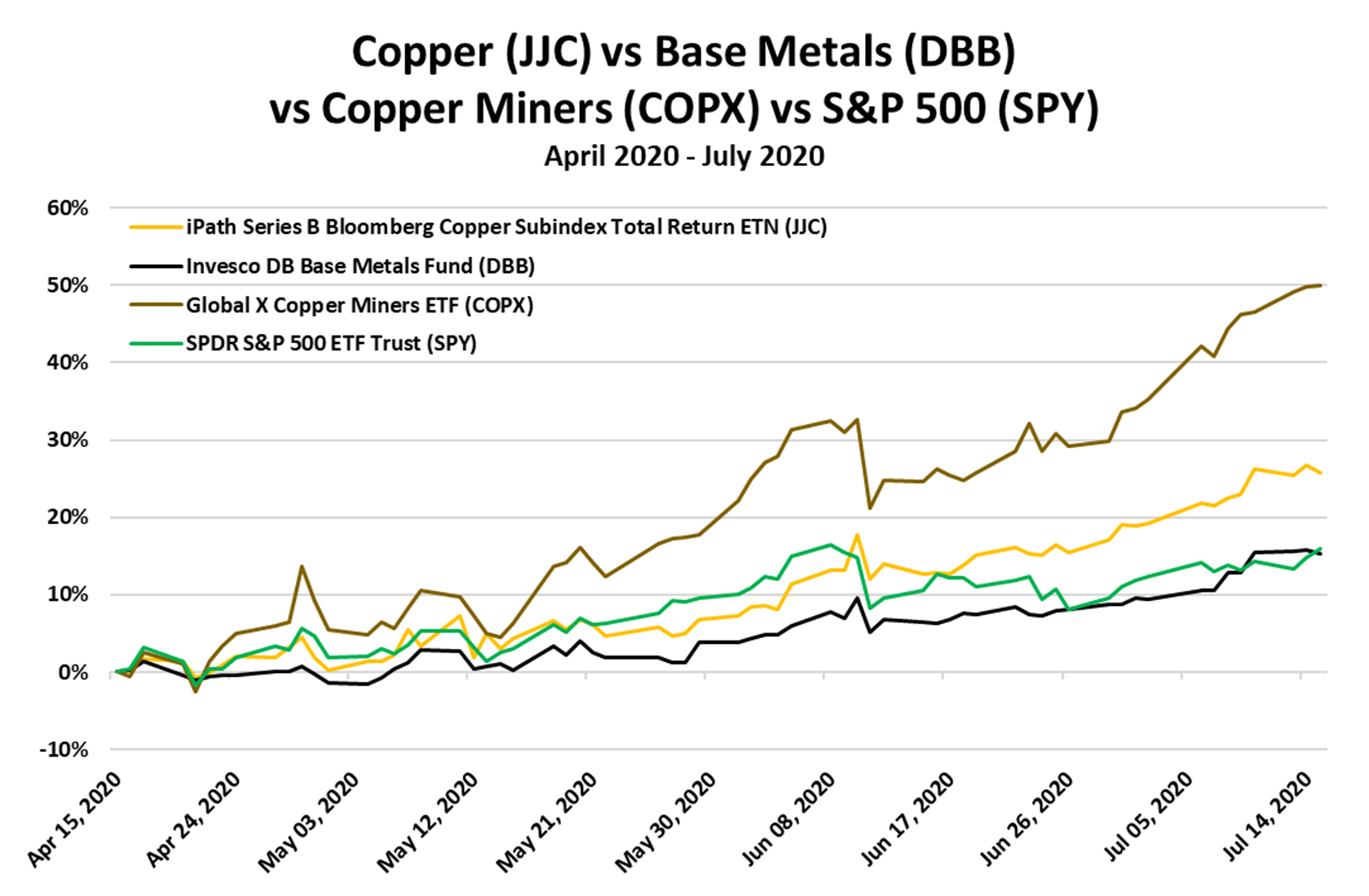

One trend in the metals category that caught our attention at the time was the dramatically shrinking global stockpiles of copper. Reduced copper supplies along with several demand-related factors have prompted MRP to turn bullish on the metal and its producers, especially now that a new economic cycle is unfolding.

That’s because copper has myriads of applications as an industrial metal. It is used in building construction, power generation and transmission, electronic product manufacturing, and the production of industrial machinery and transportation vehicles. Copper wiring and plumbing are integral to the appliances, heating and cooling systems, and telecommunications links used every day in homes and businesses. The metal is also an essential component in the motors, wiring, radiators, connectors, brakes, and bearings used in cars and trucks.

I. Post-Pandemic Recovery of the Global Economy

Industrial production is on the rise globally, as businesses resume their operations. This week’s data release from the Fed showed that U.S. industrial output surged 5.4% in June, the most since December 1959, and beating market expectations. Factory production jumped 7.2%, and even more so in the beleaguered auto industry, where production of cars and auto parts surged 105%.

A similar comeback in industrial production is taking place in in China, and in the European Union. China's industrial production rose by 4.8% from a year earlier in June 2020, marking the third back-to-back month of expansion and the largest increase in six months.

This rebound in manufacturing is positive for copper demand, as those three markets -- China, the EU, and the U.S. -- account for 80% of the world’s annual copper consumption.

The U.S. housing market’s “V” recovery, which MRP wrote about last month, should also boost demand for copper. The fact that US homebuilder sentiment has already returned to pre-pandemic levels reinforces this point. Building construction is by far the biggest user of copper in America, accounting for about 40% of annual domestic consumption, according to data from the United States Geological Survey Mineral Commodity Summary for 2018. Copper is utilized in wiring, plumbing, weatherproofing and many other construction components.

II. Global Transition to Low Carbon Economy From a longer-term perspective, copper stands to be a big beneficiary as the world transitions to a low-carbon economy. Renewable systems use about five times more copper than conventional energy systems. Electric vehicles also require 2-4 times more copper than internal combustion-engine (ICE) vehicles. For context, the average ICE car contains 1.5 kilometers (0.9 mile) of copper wire, and the total amount of copper ranges from 20 kilograms (44 pounds) in small cars to 45 kilograms (99 pounds) in luxury and hybrid vehicles.

EV sales and the switch to renewables are bound to accelerate as many countries, especially in Europe, place a green recovery at the center of their stimulus packages. Accordingly, copper could enjoy a huge demand boost in coming years, given its potentially expanding role in a green economy. The metal is considered a critical component in practically all green tech, from electric vehicles to wind- and solar-power technology.

III. The Supply Picture

On the supply side, analysts are projecting shortages in the future due to a dearth of investments in new mines. More recently, the pandemic’s rapid spread across Latin America and worker strikes have led to supply disruptions in key copper-producing nations like Chile. That’s likely to result in lower production this year.

With output from some mines limited and demand picking back up, global copper stockpiles have been dropping again since March. Inventories of copper in warehouses monitored by the Shanghai Futures Exchange stood at 137,336 tonnes on Friday, which is 64% lower than the peak of 380,000 tonnes reached around March 13. In LME-registered warehouses, copper inventories have fallen to 197,850 tonnes, down about 28% since March 13. |