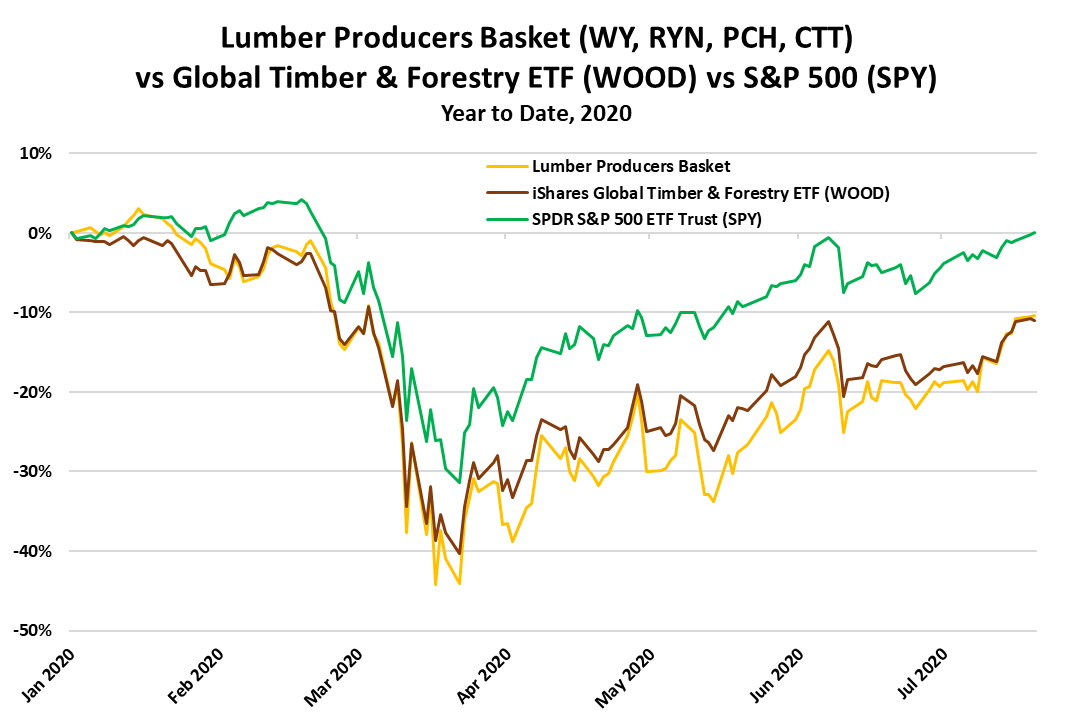

2020 could prove to be a breakout year for timber and lumber REITs as rising lumber prices, increased demand for the commodity, tight supplies, and low interest rates drive share prices higher.

Surging Lumber Prices After plunging from a spot price of $460 per 1,000 board feet on February 20 to about $260 on April 1, lumber has firmly climbed back up and is now trading around $500. The current price is 28% higher than at the beginning of 2020 and 51% higher than a year ago.

MRP believes prices could head even higher and perhaps surpass the record peak of $659 reached in May 2018 due to improving demand/supply fundamentals.

Improving Demand Fundamentals

The fact that, 50% of U.S. softwood lumber consumption is typically from homebuilders, that wood demand is highly correlated with the strength of the housing market, and that U.S. housing is weathering this year’s economic downturn a lot better than most had anticipated are reasons to be bullish on the commodity.

For one, America’s homebuilders may have just experienced their strongest June sales since the last housing boom. According to a monthly survey conducted by John Burns Real Estate Consulting, which has historically mirrored the U.S. Census report, sales of newly built homes jumped 55% annually last month, notching the largest annual gain since homebuilding began again following the housing crash a decade ago. June’s gains would come on top of May’s 12.7% year-on-year sales jump.

Industry experts credit this construction rebound to the perfect storm for the nation’s homebuilders: A sharp decline in the supply of existing homes for sale, increasing consumer preference for brand-new, high-tech homes with all the amenities for working and schooling, as well as an accelerating flight to the suburbs and exurbs following the coronavirus pandemic.

Another unexpected development has been the surge in home improvement projects this year. In the wake of the lockdowns and with many Americans spending more time at home, decks have become the new hot pandemic project. Apparently, Do-it-Yourself (DIY) demand has not abated much as states reopen, and construction demand has far surpassed lumber mills’ projections.

A race among restaurants and bars to install outdoor seating areas has been another surprising source of demand this year. In places like New York City and New Jersey, where indoor dining is still forbidden but outdoor service is allowed, bars, restaurants and cafes have been slapping together outdoor seating in bids for survival. Some places have simply encircled street parking with plywood planters, while others have gone and built entire decks.

Improving Supply Fundamentals Tight supplies are the other side of this equation. When COVID-19 entered the picture and shut down most sectors of the economy, lumber producers experienced a sudden collapse in demand. Many mills -- projecting that homebuilding would be adversely affected for a long period, and attempting to comply with goverment-mandated stay-at-home orders and social distancing measures -- decided to shut down temporarily. Accordingly, mills that remained operational substantially decreased capacity utilization.

Lumber producers had not anticipated the “V” recovery we are currently witnessing in homebuilding, nor the massive uptick in demand from do-it-yourselfers and big box retailers throughout the pandemic, and certainly not the recent push by restaurants around the country to install outdoor seating areas.

Decreasing production capacity just as wood consumption was about to surge has resulted in a dislocation of the usual supply/demand equilibrium in the lumber market. Treated wood is selling out so quickly across North America that lumber yards and other middle men have to search beyond their usual sources to replenish depleted inventories.

Catalyst for Timber & Lumber REITs

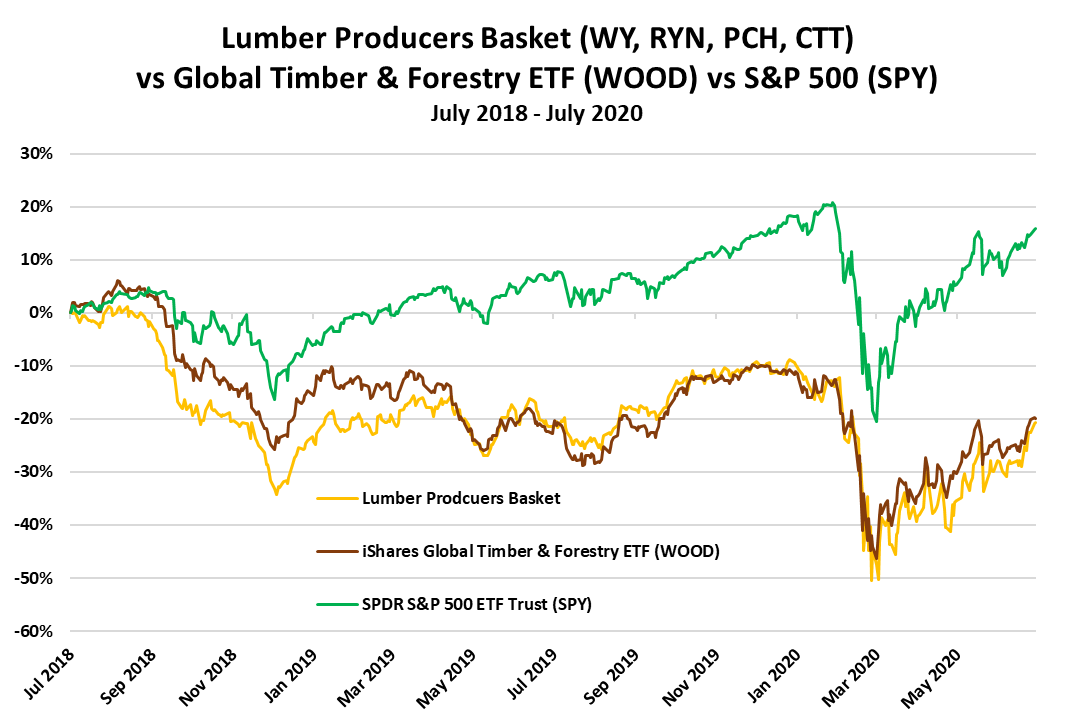

The improving demand/supply fundamentals are a boon to timber and lumber producers, particularly those that operate as real estate investment trusts (REITs). Timber REITs own and operate land that is used for the production and harvesting of timber. They make most of their money by selling raw timber that will later be converted into refined wood, or wood-based products. Lumber REITs own and operate manufacturing facilities that process the timber into beams or planks that are then sold for commercial use such as construction.

Like other high-dividend-paying stocks, REITs are largely sensitive to interest rate movements. In times of rising interest rates, the yields on REITs start to look less attractive relative to those of fixed-income alternatives. Conversely, falling or stable interest rates are beneficial to REITs. The current macro environment is supportive of REITs given that short-term interest rates in the US are close to zero, and the Chairman of the Federal Reserve has essentially told markets that rates are not moving higher any time soon.

How to Invest

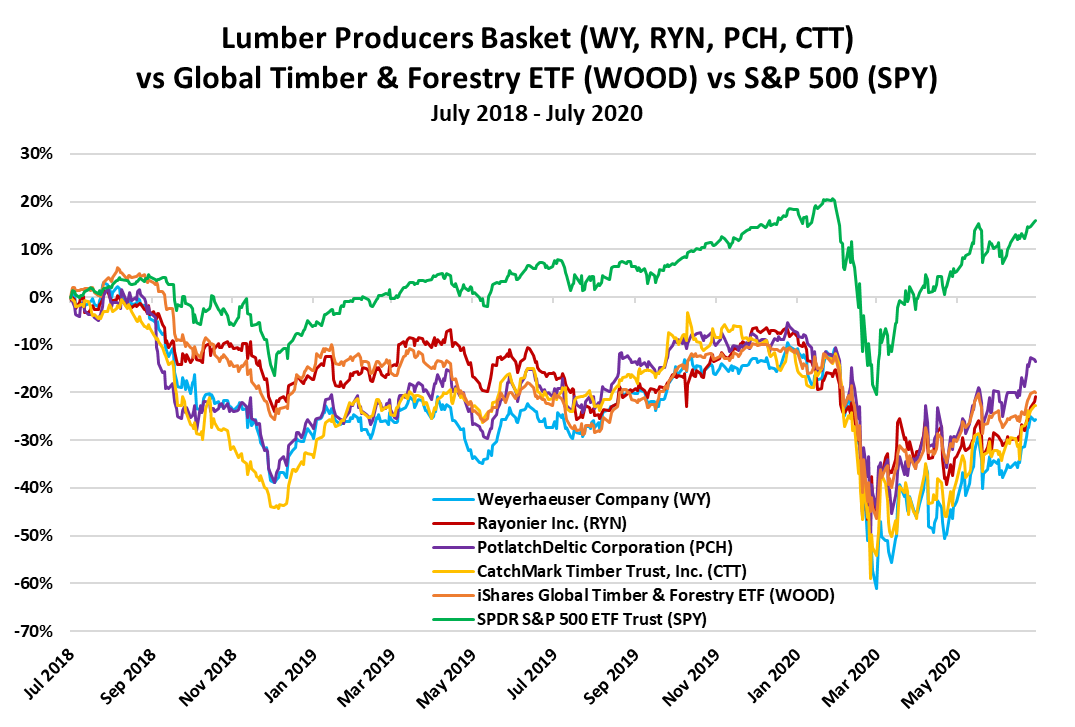

There are four publicly-traded U.S. REITs that specialize in the timber and lumber category.

Weyerhauser (WY), which operates both as a private owner of timberlands and as a manufacturer of lumber & engineered wood, is considered the industry leader. The company owns over 12 million acres of timberlands in North America and runs some of the lowest-cost wood products manufacturing facilities in the industry.

Rayonier (RYN), the second-largest REIT in this space, is more of a pure-play on the raw commodity. The company harvests and sells timber from its land and tries to extract maximum value in other ways, however it does not have a manufacturing operation.

PotlatchDeltic Corp (PCH) was formed following the 2018 merger of Potlatch and Deltic, two timber companies that were looking to create one stronger entity. The result of that union is a diversified timber & lumber company that owns nearly 2 million acres of timberlands and a large manufacturing business that produces lumber and plywood.

CatchMark Timber Trust (CTT), the smallest and youngest REIT in this group, owns about 1.6 million acres of timberlands located primarily in the Southern United States. Over 1 million of these acres are in Texas, however the company has started to diversity into the Pacific Northwest.

Investors seeking exposure beyond North America can turn to ETFs like the iShares Global Timber & Forestry ETF (WOOD). The fund invests in a geographically diverse portfolio of companies whose fortunes rise and fall with lumber’s price

|