The spot price for U3O8 (triuranium octoxide, the most stable form of uranium oxide found in nature) moved above $30 per pound for the first time this year. As Mining.com reports, two new research notes from BMO Capital Markets and Morgan Stanley say today’s price marks a floor and predict a rally in prices over the next few years to the $48 – $50 level by 2024.

Supply Shrinkage Continues On

Those predictions come as several key uranium firms have finally seen success in thinning out a global glut of supply that forced prices below the $20 level in the mid-2010s. While estimating the exact global stockpile is tricky, the Wall Street Journal notes there are some indications that inventory is starting to get depleted. Over the past five years, roughly 815 million pounds of uranium oxide equivalent have been consumed in reactors, while 390 million pounds have been locked up under long-term contracts with the uranium producers, according to UxC’s estimates.

After years of cutting mining operations, the annual global supply deficit of uranium is projected to average a total of 23 million pounds through 2022, or roughly 13% of global uranium demand, according to Scotia Capital.

As FNArena reports, two more mines closed indefinitely in the first quarter 2021: Energy Resources of Australia’s (ERA) 3.5 million pound Ranger mine ended production in January, while Niger's 2.6 million pound Cominak mine shut at the end of March. Morgan Stanley analysts forecast total mine supply to increase 10% in 2021, rebounding from a year of COVID-19 shutdowns, but that will still fall -6% short of 2019 levels.

Without a significant price appreciation soon, more mines will likely shut and some project downstream development will slow even further.

As Uranium fund Sachem Cove Partners’ CIO Mike Alkin stated last year, “If prices stay below $50 per pound, idled production won’t come back online and new mines won’t get built — that need to get built — and deficits will be at least 35 million pounds per year” out to 2030.

Per MRP’s March report on uranium, COVID-19 hit the uranium industry hard, forcing the idling of much more capacity than planned – including two separate shutdowns of Cameco’s Cigar Lake facility, the largest source of uranium in the world.

Cigar Lake had produced just 2.3 million pounds of uranium oxide in the January-September 2020 period, way below its target for the 2020 year of 5.3 million pounds. The facility’s mining operations have been shut since December.

Worldwide production declined 30% due to the COVID-19 pandemic, notably in Kazakhstan which produces 40% of the world’s uranium.

Firms Rush to Scoop Up Spot Market Sales

Cameco later poured fuel on the fire when said it will go into the spot market to buy uranium oxide to meet the totals for its sales agreements, adding further upward pressure to prices.

That purchase was a sign of more to come, as market activity has been particularly strong through the first quarter of 2021. Even with uranium prices bouncing back, purchasing product in the spot market remains cheaper than the cost of production. Many firms see this as an opportunity to build up an affordable strategic inventory that will benefit their balance sheets as long-term investments, as well as help to continually dry up the spot market.

Denison Mines Corp. said this month that it has secured 2.5 million pounds of uranium concentrates at $29.61 a pound at a total cost of US$74 million. The purchase is an obvious bet that uranium prices will rise. As Resource World notes, all of the purchases were made on the uranium spot market, with delivery dates ranging from April 2021 to October 2021.

Per World Nuclear News (WNN), Western Australia’s Boss has entered into binding agreements to purchase 1.25 million pounds U3O8 on the spot market at a weighted average price of $30.15per pound, and is funding this by a "well-supported" AUD60 million share placement. Boss will acquire the first 0.25 million pounds by the end of April and the remainder by the end of June.

In an especially large transaction, UK-based uranium purchaser Yellow Cake PLC elected March 15 to fully exercise its $100 million uranium purchase option for 2021 with JSC National Atomic Co. Kazatomprom and agreed to purchase another 440,000 pounds from the Kazakh uranium major. As S&P Global notes, the move may prompt Kazatomprom, the largest uranium producer in the world, to purchase material on the spot market to fulfill outstanding contracts.

WNN reports that US uranium producer UEC entered into initial agreements totaling $10.9 million to purchase 400,000 pounds of US warehoused uranium. Per UEC CEO Amir Adnani, this initiative will support three objectives: to bolster UEC's balance sheet as uranium prices appreciate; provide a strategic inventory to support future marketing efforts with utilities that could compliment production and accelerate cashflows; and increase the availability of production capacity from the company's Texas and Wyoming operations.

US Stacks up a Stockpile, China Ramps Up Reactors

Freeing up production capacity is a key goal for Uranium Energy Corp. (UEC), since they are one of the companies that will be supplying the US’s new federal uranium reserve. As MRP previously noted, congress approved $75 million for an initial year of funding for the reserve, resulting in a 2.5 million pound purchase of American uranium, according to Investor Intel. That amount is well-above annual domestic production, which was only 174,000 pounds of U3O8 (uranium oxide concentrate) in 2019 and declined even further in 2020.

The World Nuclear Association estimates roughly 50 nuclear reactors are being constructed in 16 countries compared with about 440 operating today. That includes substantial capacity in China, perhaps the most important market for the future of nuclear energy.

Last month, China unveiled its 14th five-year economic plan, which includes plans to increase nuclear power capacity from 48 gigawatts presently, to 70GW by 2025. In late 2020, MRP noted that China aims to become one of the world’s largest nuclear power users, planning to build over 80 new reactors in the next 15 years, and more than 230 by 2050.

China currently operates 47 nuclear plants with a total generating capacity of 48.75 Gigawatts (GW) — the world’s third highest after the United States and France.

For Investors

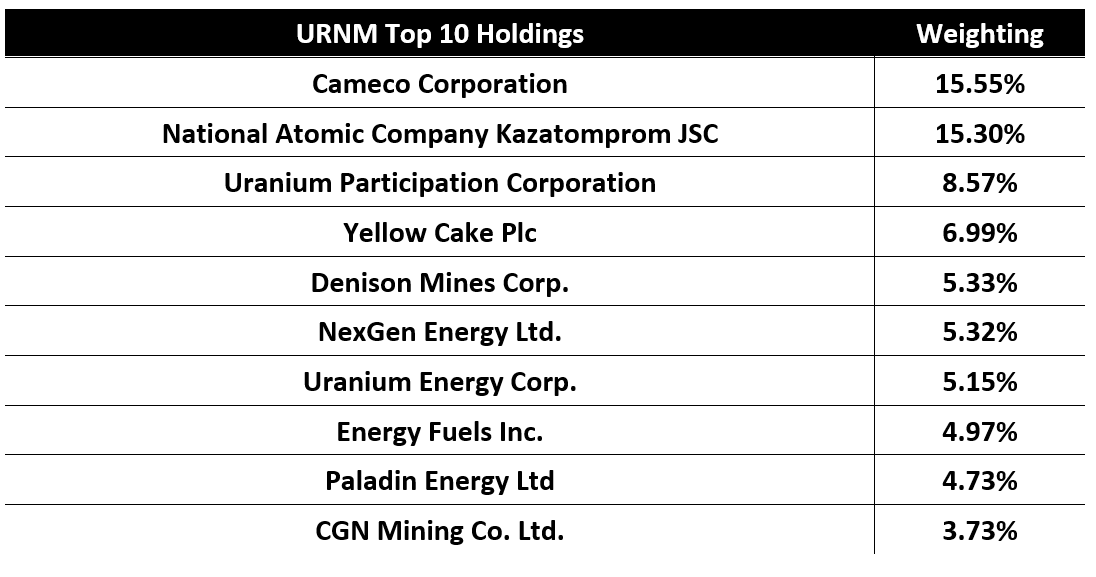

Investors seeking to capitalize on the opportunity have several ETFs to choose from. One of these is the North Shore Global Uranium Mining ETF (URNM), which invests in a basket of global companies involved in the mining, exploration, development and production of uranium, as well as companies that hold physical uranium.

URNM launched in December 2019, so it is a relatively new ETF with about $ 116 million in net assets. It is a pureplay on uranium miners, unlike the older and larger Global X Uranium ETF (URA) which combines uranium miners with nuclear component producers.

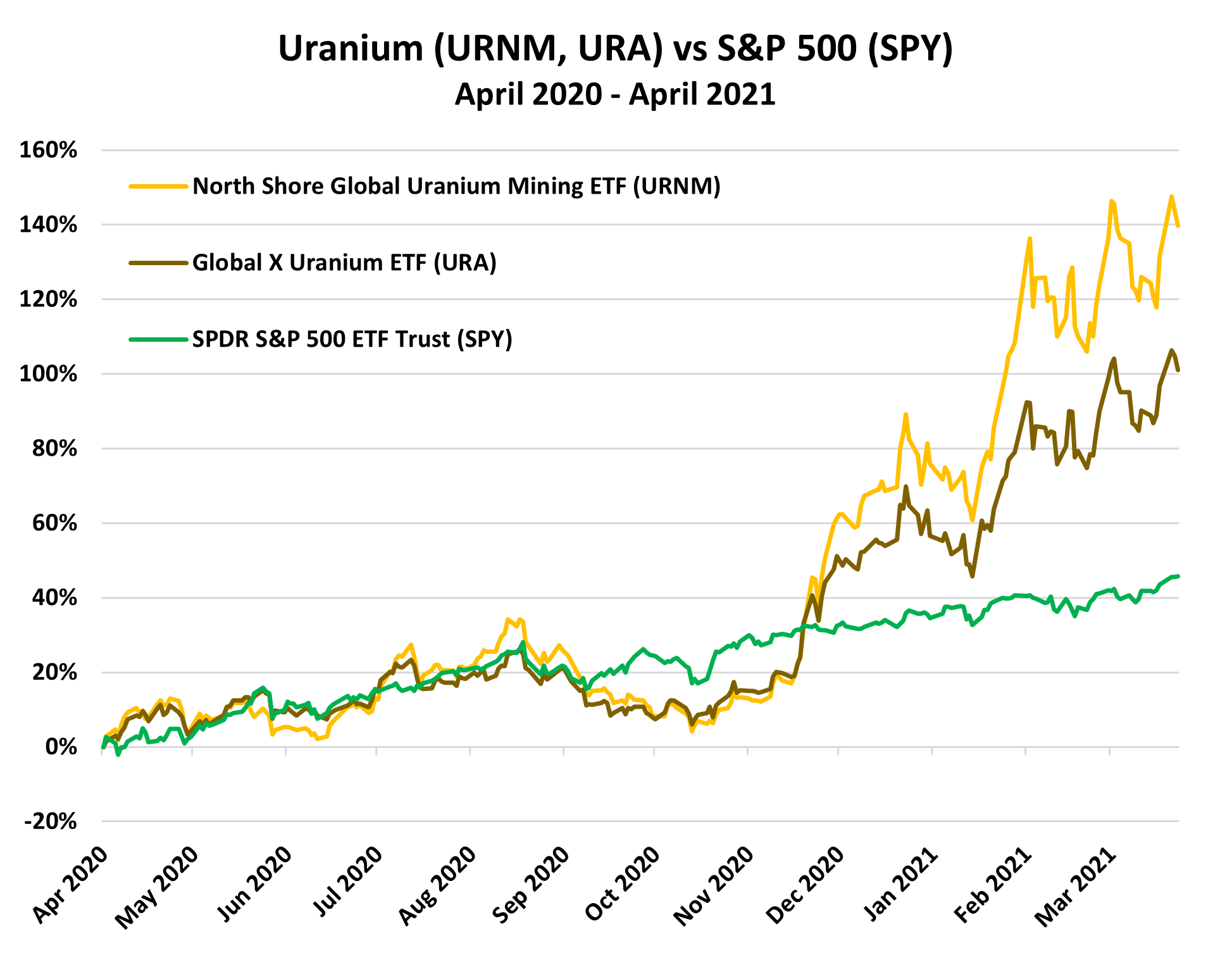

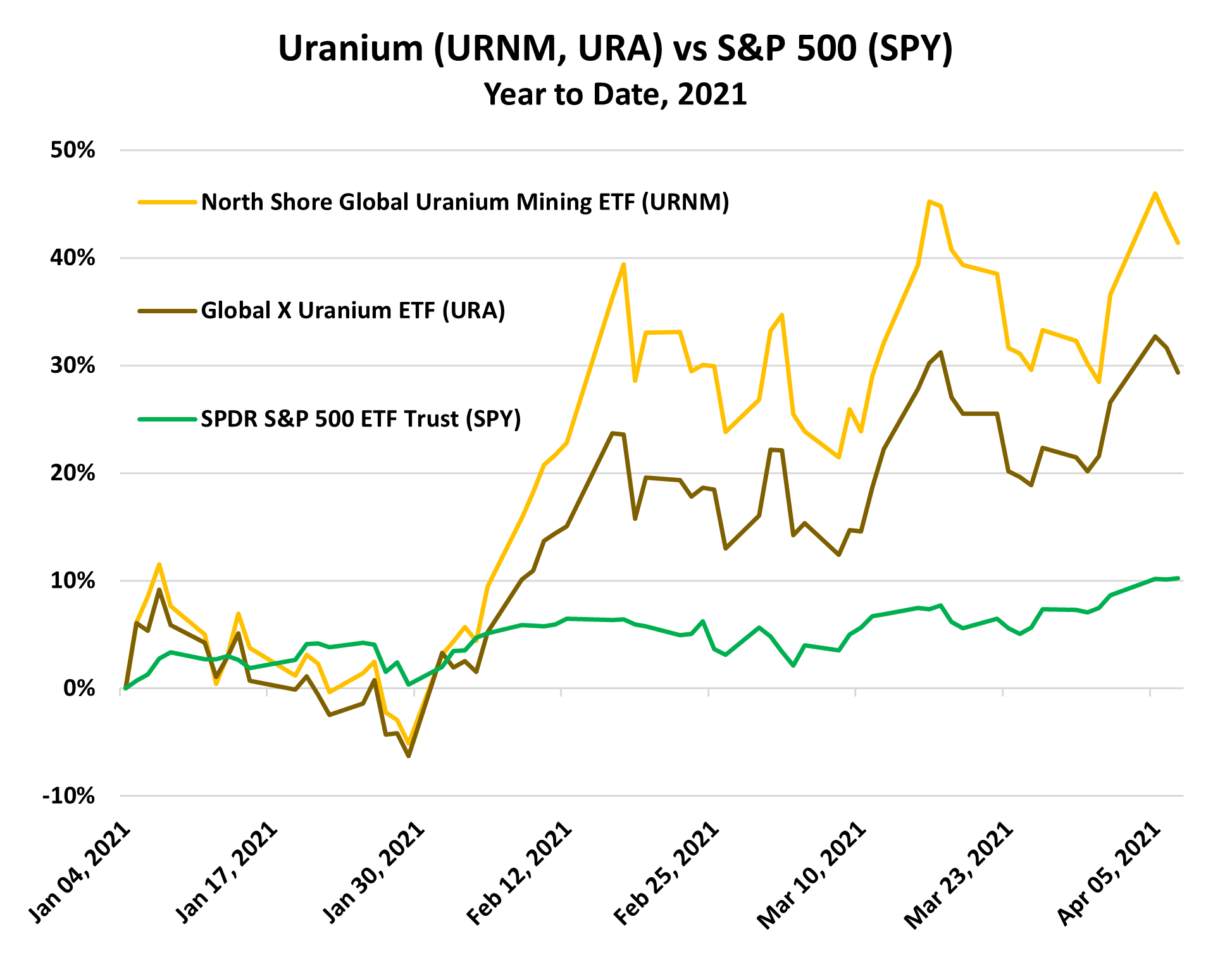

In our April 16, 2020 report on uranium, MRP wrote: “An ongoing supply shock is moving the uranium market’s demand/supply balance in favor of miners”. Since the publication of that report, the North Shore Global Uranium Mining ETF (URNM) has returned +140%, more than tripling the S&P 500’s +46% gain over the same period. |